In-Use

Information correct as of 9thJuly 2026. Please see kb.breeam.com for the latest compliance information.

Acoustic sample testing approach – calculation procedure - KBCN1675

The methodology sets out a sample testing approach which can be applied to group rooms into those of similar room type or performance requirement category or construction type.

Where rooms are grouped to the same use and construction for instance, only 1 in 4 pairs of adjacent rooms would need to be tested, and the results would be representative of all similar rooms e.g. where there are 12 pairs of similar offices and 3 are tested and are compliant, all 12 would be deemed compliant (or 100%).

Therefore, it is not a requirement to test 80% of the rooms to be 80% compliant for those projects where a sampling approach can be applied.

Alarm systems – Intent of Criterion 2 - KBCN1707

The intent of Criterion 2 is as follows:

A documented plan is in place to ensure that when the alarm is triggered, whether due to a fire or security incident, a system fault or a false alarm, building staff and occupants understand what actions to take. This must include any necessary communication with ARC staff, emergency services and other building users.

This clarification will be incorporated in the next update of the technical standard.

29 April 2025 - Due to the ambiguity of the guidance in technical manual, where project teams demonstrate that the assessment documentation was prepared prior to the publication of this KBCN, and that the wording of criterion 2 in the technical manual has been followed, this KBCN can be disregarded.

Alternative methods for ensuring the re-use or recycling of materials - KBCN1150

In a scenario where management processes result in the recycling or re-use of a waste stream, this can be considered as one additional compliant waste stream within the question. For example, sites where a take-back scheme is utilised with installers/manufacturers for a particular waste stream, and the manufacturer re-uses or recycles this off-site.

In order for this to be compliant the following must have been met:

- The Assessor must clearly outline the waste stream which is being recycled/re-used

- The Assessor must clearly outline the process which occurs, including: (a) How the waste leaves the site, and (b) What happens to the waste after it leaves the site

- If the waste is transferred to another party (such as a supplier in a take-back scheme), there needs to be evidence of a current valid agreement/contract in place outlining that this service will be provided for at least 12 months.

- All relevant legislation is complied with.

- This should be a regular occurrence of waste, and subsequently should be collected at least once a month.

- If the waste remains on-site temporarily before it is removed, the waste should therefore be stored in line with the assessment criteria outlined in WST 01.

Note: it is

not possible to award credits for the same waste stream twice. For example, a take-back scheme for cardboard, as well as a recycling point for cardboard in the centralised waste storage location, can only be considered to be one waste stream.

Amenities – Assessed building is one of the listed amenities - KBCN0264

Where the assessed building is itself included in the list of amenities, that particular amenity criterion can be deemed to be met, e.g. a supermarket development itself meets the proximity to food outlet required for a Retail type building.

Applicability – Management – common areas only assessment - KBCN1559

Principle

In an assessment of common areas only, building management are still responsible for the common welfare all users and for policies governing the overall asset.

Evidence

For assessments of common and tenanted areas, the scope of the manual states:

“The assessment must include evidence of a representative sample of the tenants to ensure that central management practices are in place and fully implemented in line with the assessment criteria.”

For assessments of common areas only, evidence is required from building management only.

| Issue |

Scope of issue |

| Part 2 |

| Man 01 Building user guide |

No change to the criteria or evidence requirements.

A building user guide is required regardless of scope. |

| Man 02 Management engagement and feedback |

No change to the criteria or evidence requirements.

Engagement with building users is required regardless of scope. |

| Man 03 Maintenance policies and procedures |

Applies only to core systems which serve the common areas and are maintained by the building management. This includes any core systems which also serve tenanted areas (for instance, asset-wide ventilation systems) where this cannot be separated from tenanted space. |

| Man 04 Environmental policies and procedures |

Applies to asset-wide environmental policies only.

Answer D can apply to improvement targets for common areas only, where this can be separated from tenant targets. |

| Man 05 Green lease |

Where there are tenants occupying the asset, this issue is not filtered out.

Consideration of green contracts are within the control of building management regardless of scope. |

Applicability – no occupied spaces - KBCN1551

Principle

Where:

- The scope of assessment covers no occupied spaces and,

- There is no valid way to filter credits from that issue,

Credits specifically related to occupied space are not awarded.

Outcome

The tables below show how this principle applies to affected issues.

- Y means all credits are available (unless the comments state otherwise).

Standard filtering rules still apply, so some credits can be filtered out where allowed in the criteria.

- N means all credits in the issue cannot be awarded.

These credits are not filtered out.

| Issue |

Credits available |

Scope |

| Part 1 |

|

|

|

| Hea 01 Daylighting |

Y |

|

Only answer C is available. |

| Hea 02 Control of glare from sunlight |

|

N |

|

| Hea 03 Internal and external lighting levels |

|

N |

|

| Hea 04 Lighting control |

|

N |

|

| Hea 05 Minimising flicker from lighting systems |

Y |

|

|

| Hea 06 View out |

|

N |

|

| Hea 07 User comfort control |

|

N |

|

| Hea 08-13 |

Y |

|

|

| Part 2 |

|

|

|

| Hea 14 Thermal comfort |

|

N |

|

| Hea 15 Smoking policy |

Y |

|

|

| Hea 16 Indoor air quality management |

Y |

|

|

| Hea 17 Acoustic conditions |

|

N |

|

| Hea 18 Legionella risk management |

Y |

|

|

| Hea 19 Drinking water management |

Y |

|

|

16-Dec-2022 - KBCN title and scope updated for better visibility. Error in Hea 03 amended. Applicability of KBCN applied only to affected issues (N, or modified answer options) with to minimise header space in the UI. Original content on Resources moved to new KBCN.

27-Nov-2025 - KBCN applicability updated to include all Hea credit issues.

Applicability – Resources – common areas only assessment - KBCN1557

In an assessment of common areas only - the scope of some issues are modified in the table below.

Answers which are unavailable cannot be filtered out, and cannot be awarded by default.

| Issue |

Scope |

| Part 1 |

|

| Rsc 02 Reuse and recycling facilities |

Answers D and E are only available if occupants store waste in a central waste storage facility within the assessed common area. All other credits are available. |

| Part 2 |

|

| Rsc 06 Optimising resource use, reuse, and recycling |

Answer D is only available if occupants store waste in a central waste storage facility within the assessed common area. All other credits are available. |

Applicability – tenanted assets with common areas - KBCN1593

Principle

- Waste generated in common areas is the responsibility of building management.

- Waste generated in tenanted areas is the responsibility of the tenant.

- The asset as a whole meets the aim and criteria of the issue.

Common areas

Common areas must include:

- Bins for general waste AND

- Bins for recycable waste.

Segregated or commingled.

Mixing recyclable and non-recyclable waste in one bin is not acceptable, even if recyclable content is extracted later from the mixed waste.

If the recyclable waste is commingled, the waste collector demonstrates that they separate commingled waste in the minimum number of waste streams defined in the methodology.

Tenant or building management controlled areas

The issue criteria can be met through multiple storage areas, or a central store.

Where there are multiple storage areas, the space requirements for Answer C or D can be calculated based on the combined area of all storage areas.

The waste storage area requirements for tenants and building management must be calculated separately as stated in the manual.

Apportioning Water Consumption – common areas only assessment - KBCN1679

For assets where only the common areas are being assessed, the water consumption targets and actual figures reported should be based on the water used within the assessed areas only.

Therefore, where metering is provided for the whole building consumption and no separate metering of common areas is available, a logical assessment of the sanitary (and other) water use and distribution should be carried out so that the figures are based on an accurate estimation of water usage within the common areas. Apportioning must not be based purely on the percentage of floor area.

A logical assessment could be based, for example, on the percentage of water using equipment installed, such as the proportion of toilets/taps/dishwashers etc within the scope of the assessment against those outside of the scope.

Justification and calculations should be provided within the evidence to support the reported figures.

Approved Equivalent Roles List (AERL) - KBCN1809

BREEAM International standards are unique because of their flexibility.

For International projects, Assessors can submit roles to substitute those described in the Technical Manuals. Provided that such roles are equivalent to the BREEAM specified roles, BRE Global will approve them for use in a particular country or region.

The

Approved Equivalent Roles List is a record of all roles that BRE Global has approved to date. The list is periodically updated to reflect recent approvals or withdrawals.

Using existing approved roles

Where you are using an approved role, and not the role described in the criteria in the scheme Technical Manuals, a copy of the AERL should be included as part of your evidence submission for QA.

AERL versions

The version of the AERL that is current at the time of registration is the one that is used for assessment. Newer versions released after this can also be used, however older versions before the registration date cannot be used.

For example: if the version current at registration was v3.0, then v3.0 (or any later versions) can be used, but v2.0 (or any earlier versions) cannot be used.

Proposing new roles

New roles cannot be proposed if they are not of equal competency to the BREEAM requirements. Only roles which are equivalent or more rigorous than the BREEAM default roles are considered.

If you wish to propose a new role which you think is equivalent in your country or region:

- Check what the role needs to cover by referring to the roles described in the scheme Technical Manual definition.

- Complete BF2599 BREEAM Approved Equivalent Roles Application Form and send this to our Technical Team via the Query Webform, adding AERL into the subject field.

The information provided to us within this form must include:

- the names of the proposed role(s)

- confirmation of the scheme and issues the role should apply to

- confirmation of the roles / competent persons you are referring to in the manual

- a detailed explanation of how this work is conducted in your market and how it meets the same level of competency as the BREEAM requirements

- documentation to support your explanation which is clearly marked for our ease of reference. If the documentation is not in English, translations of the relevant sections must be provided.

We will need a few weeks to review the information (please check with us for time scales). If there is missing information, or the information is not clearly referenced, this might take longer.

If successful, we will send you a revised copy of the AERL which includes the new role, and will update this for future versions of the AERL.

Assessing industrial spaces – exemptions - KBCN0734

The thermal comfort criteria do not apply to the operational or storage areas typically found in industrial assets or other similar asset types. The criteria is still be applied to the other parts of the asset as appropriate.

Operational and storage areas often have function-related thermal requirements determined by operational or storage needs. These functional requirements override the needs of any occupants.

17-Jan-2024 - Scheme applicability updated.

03-Nov-2020 - Issue 2.0 of UK RFO technical manual updated with new CN detailing the above.

Assessing multiple buildings in BREEAM In-Use 2015 - KBCN0840

BREEAM In-Use has been developed as an environmental assessment method to assess existing assets. Typically, an asset consists of a building or part of a building. In certain circumstances, multiple buildings can be classified as a single asset by a client. This is often the case where buildings are of similar physical structure and built form, have common building servicing strategies and common management arrangements.

To assess multiple buildings as a single asset using BREEAM In-Use, the criteria listed below must be confirmed by a licenced BREEAM In-Use Assessor. This will ensure a meaningful outcome of the performance of the asset.

- All buildings must have the same building function, similar performance, and be of the similar design and age.

- Buildings must either:

- Be connected to and share common services to meet the comfort and sanitary demands of the occupants. This includes: heating, ventilation,cooling and hot water.

- If these services are provided locally: identical servicing strategies as well as specification of equipment must be applied across all buildings.

- All buildings must share similar building envelope (the physical separator between the interior and exterior of a building) and structural specifications. Buildings do not need to be physically connected, however: the specification of the envelope must be largely the same to ensure that the performance of each building fabric is comparable in terms of the range of assessed characteristics including thermal efficiency.

- Building management and maintenance policies, procedures and approach must be the same across all the buildings that make up the asset to ensure consistent implementation.

- All buildings must be located on the same site. The boundary of the site must be drawn where responsibility of management or ownership of the site changes.

- The Assessor must collate the required evidence from each building that is included in the asset and where performance against the BREEAM requirements varies, the final score will be determined by the space with the lowest level of performance.

- If alterations are made to the management and the physical structure of the asset that in turn changes the applicability of the eligibility criteria above, re-certifications must be undertaken at a building level if the Multiple Buildings approach is no longer applicable.

Please note: if the buildings differ from each other in a number of areas, a multiple buildings approach has limited value to all parties involved. In such cases, the rating will not clearly identify the areas for improvement within each building. By assessing the buildings separately, the granularity of the assessment is increased which will in turn provide owners with more detailed information on how improvement plans can be rolled out.

For assessment multiple buildings under BREEAM In-Use Version 6, please see:

09 Aug 2024 - Title updated. Reference and links to guidance for current BIU standards added

Assessing multiple commercial buildings - KBCN1686

BREEAM In-Use has been developed as an environmental assessment method to assess existing assets. Typically, an asset consists of a single building or part of a single building. However, BREEAM In-Use provides an exception where certain criteria have been met, and this is set out in the relevant Technical Manual under the Eligibility Criterion 5 and reproduced below with clarifications noted in Italics.

The requirements to assess multiple buildings as a single asset

Criterion 5 states: An asset cannot normally include more than one building. The only exception is where several buildings meet the following criteria:

a) All buildings must be located on the same site. The site boundary must be drawn where responsibility for management or ownership of the site changes.

The site interior may include public roads, such as industrial or office business parks, but the properties on which the buildings sit must otherwise be contiguous.

b) All buildings must have the same building function, similar performance, and be of similar design and age.

This includes Subtype as well as Type. For example, three Industrial buildings, all of which function as warehouses, could be grouped. However, if one is a cold storage facility, another is advanced manufacturing, and the third is warehousing, this would not be acceptable.

c) Building management and maintenance policies, procedures and approach must be the same across all the buildings that make up the asset to ensure consistent implementation.

Where maintenance policies, procedures, and approaches are the tenant’s responsibility through the leasing arrangements (for example, in industrial properties), these can vary, but overall building management needs to be the same for all properties.

d) Evidence must be collated from each building that is included in the asset and where performance against the BREEAM requirements varies, the final score will be determined by the space with the lowest level of performance.

The whole data set for all buildings in the assessment must be gathered and provided to the Assessor by the Client.

Demonstrating compliance for certification

- The Client will be required to demonstrate how each criterion has been met and provide evidence to support the approach.

- The Assessor must then confirm the criteria have been met through their evidence review and on-site verification.

- Site level assessments, such as an outdoor retail asset, should use a floor-area-weighted average method to confirm compliance.

- For other commercial assessments involving multiple buildings, representative sampling is permitted to confirm compliance. Assessors are required to confirm that the worst-case performance was applied by the Client. Assessors are required to create and document a robust representative sampling method and demonstrate that they conducted their assessment in accordance with their methodology.

- Where the Assessor is unsure how to interpret or apply the criteria, they should contact the Technical Team for clarification using the BREEAM Projects webform before submission for certification. Where relevant, a copy of the technical clarification response should be submitted as supporting evidence.

Considerations before undertaking this approach

- The rating will reflect the worst performance of all the buildings included within the assessment.

This will limit the visibility of buildings within the grouping that may have better performance and opportunities at individual assets to improve performance. Assessing the buildings separately allows for the granularity of the assessment to provide owners with more detailed information on how improvement plans can be rolled out and the value to be gained from driving performance.

- Should the buildings be sold individually, the certification status does not transfer with the individual buildings.

The building(s) sold would need to undergo the full certification process, including benchmarking and the on-site visit with a licensed Assessor, to be considered certified and claimed by the new ownership.

- The certificate may be updated through a mid-cycle process to remove the assessed area of the building(s) sold.

This could increase the score if the building sold represented the worst-case performance. If the building removed from the certification formed the basis of the score as the 'worst-performing', the Assessor would need to complete another site visit for the mid-cycle to ensure that the new data representing the worst performance is accurate.

Assessing multiple residential buildings - KBCN1687

BREEAM In-Use has been developed as an environmental assessment method to assess existing assets. Typically, an asset consists of a single building or part of a single building. However, BREEAM In-Use provides an exception where certain criteria have been met, and this is set out in the relevant Technical Manual under the Eligibility Criterion 5 and reproduced below with clarifications noted in Italics.

The requirements to assess multiple buildings as a single asset

Criterion 5 states: An asset cannot normally include more than one building. The only exception is where several buildings meet the following criteria:

a) All buildings must be located on the same site. The site boundary must be drawn where responsibility for management or ownership of the site changes.

For multifamily assets, this means all structures within the property boundary.

For individual homes, e.g. single family, townhouses, this means the properties on which the homes are located are contiguous.

b) All buildings must have the same building function, similar performance, and be of similar design and age.

Multifamily projects, such as garden style apartments, can still be grouped together under these criteria, even if they include different unit types.

c) Building management and maintenance policies, procedures and approach must be the same across all the buildings that make up the asset to ensure consistent implementation.

Where maintenance policies, procedures, and approaches are the tenant’s responsibility through the leasing arrangements, these can vary, but overall building management needs to be the same for all properties

d) Evidence must be collated from each building that is included in the asset and where performance against the BREEAM requirements varies, the final score will be determined by the space with the lowest level of performance.

The whole data set for all buildings in the assessment must be gathered and provided to the Assessor by the Client.

Demonstrating compliance for certification

- The Client will be required to demonstrate how each criterion has been met and provide evidence to support the approach.

- The Assessor must then confirm the criteria have been met through their evidence review and on-site verification.

- Site level assessments should use a floor-area-weighted average method to confirm compliance.

- For other residential assessments involving multiple buildings, representative sampling is permitted to confirm compliance. Assessors are required to confirm that the worst-case performance was applied by the Client. Assessors are required to create and document a robust representative sampling method and demonstrate that they conducted their assessment in accordance with their methodology.

- Where the Assessor is unsure how to interpret or apply the criteria, they should contact the Technical Team for clarification using the BREEAM Projects webform before submission for certification. Where relevant, a copy of the technical clarification response should be submitted as supporting evidence.

Considerations before undertaking this approach

- The rating will reflect the worst performance of all the buildings included within the assessment.

This will limit the visibility of buildings within the grouping that may have better performance and opportunities at individual assets to improve performance. Assessing the buildings separately allows for the granularity of the assessment to provide owners with more detailed information on how improvement plans can be rolled out and the value to be gained from driving performance.

- Should the buildings be sold individually, the certification status does not transfer with the individual buildings.

The building(s) sold would need to undergo the full certification process, including benchmarking and the on-site visit with a licensed Assessor, to be considered certified and claimed by the new ownership.

- The certificate may be updated through a mid-cycle process to remove the assessed area of the building(s) sold.

This could increase the score if the building sold represented the worst-case performance. If the building removed from the certification formed the basis of the score as the 'worst-performing', the Assessor would need to complete another site visit for the mid-cycle to ensure that the new data representing the worst performance is accurate.

Assessments of owner-occupied or common areas only assets - KBCN0804

In situations where an asset is owner-occupied, or if there are no tenanted areas within the assessed area, it is still possible to achieve credits under MAN 11. Instead of awarding credits based on green leases with tenants, credits can be awarded based on the owner/manager having in place policies/processes outlining specific targets (considering at least energy, water and waste efficient practices) applicable to the assessed area.

With regards to the evidence required in this scenario: the assessor must submit documents (which could include, but are not limited to, contracts or policies) that outline how the owner/manager has set and measured these targets.

Assessor comments submitted within BREEAM In-Use assessments - KBCN0962

Assessor comments are an extremely important part of the certification process, and are used to give the Quality Assurance (QA) team at BRE Global an understanding on why the Assessor has awarded credits. Assessor comments must be provided for any question which has credits awarded.

The comments must provide the following information:

- Explanation on why the Assessor has deemed that the asset is compliant in relation to the credits awarded.

- Explanation on where compliance is demonstrated within the evidence which has been submitted. For example, if compliance is found within a particular section of a large document, the comments should help direct the QA team to the applicable section.

- Outline any information provided by BRE Global (external to the technical manual) which supports the decision made by the Assessor. For example, Knowledge Base Compliance Notes, or technical query responses.

In situations where the client has submitted detailed comments (on the client side of the tool) which already outlines all of the relevant information noted above, then the Assessor can simply provide a shortened comment verifying the accuracy of the client comment.

Note: Assessor comments must be written in English in order for the QA team to review the assessment. Where the majority of the information is provided within the client side, then this also needs to be in English, or simply translated over within the Assessor comments.

Example of compliant Assessor comments (related to HEA 01 – SD221 – 2.0:2015)

“2 credits have been awarded as 20% of the building envelope is glazed. Verification of this figure can be seen within the calculation provided within [insert evidence name]. Please also find photographic evidence of each side of the envelope [insert evidence name], as well as the drawings for each envelope which the calculations were based on [insert evidence name]."

Asset classification – co-living developments - KBCN1568

This guidance is intended as a general reference only. Each co-living development will include a different combination of residential accommodation and managed communal spaces. Assessors must apply professional judgement to determine the most appropriate asset classification.

Typical characteristics of co-living developments

Developments within these sectors typically include the following characteristics:

- Institutional ownership and professional management

Purpose built for rental as the primary function, rather than individual sale, and owned by a single entity with professional property management in place.

- Self-contained, functional units

Residential apartments with private kitchens and bathrooms.

- Managed communal facilities

Extensive shared amenities, such as fitness suites, co-working areas, communal terraces, and secure bicycle storage.

- Flexible, long-term tenancy

Tenancy agreements are generally designed for longer term occupation, typically six to twelve months.

Classification guidance

International assets:

The following classifications are recommended:

| Assessment Type |

Recommended Classification |

| International New Construction, International Refurbishment and Fit-Out (will become Refurbishment and Fit-out from V7 onwards) |

Residential institutions- long term Stay* |

| BREEAM In-Use (BIU) |

Residential |

*Assessors should also consider how the asset is classified under relevant local building regulations to support the interpretation of Residential Institution.

UK NC assets (KBCN1225, provides additional clarification):

Using Building Regulations classifications as a guide

- Part L, Volume 1 (Dwellings): Classified as Residential, covered under UKNCR (formerly known as HQM).

• Part L, Volume 2 (Buildings other than dwellings): Classified as a Residential Institution, covered under UK New Construction.

17-Jun-2026 - Guidance revised and updated for clarity

Asset Footprint - KBCN0664

The following guidance can now be used to interpret the meaning of the asset footprint:

Building only:

- The asset is a building on its own without any associated site attached to it (for example an office tower in a city centre). In this case, the asset footprint can be considered to be the area of the asset/building only, typically the ground floor area.

- Planting, including roof- and or vertical planting, on the asset/building that is under assessment must be included in the calculation.

Building located on a site:

- The asset footprint can be taken as the site on which the building is situated. The boundary of the site must be drawn when either:

- Responsibility of management or ownership of the site changes; OR

- If a site includes multiple assets and there is a clear demarcation of the area associated with each asset, then this must be considered to be the site boundary for the asset footprint.

- The footprint of any asset that is on the site but does not form part of the assessment will be deducted from the asset footprint.

- Planting, including roof- and or vertical planting, on the asset/building that is under assessment must be included in the calculation.

- Planting, including roof- and or vertical planting, on other assets/buildings than the one under assessment must be excluded from the calculation.

Calculation methodology for LE01

Percentage planted area = [Total area planted (m²) / Asset footprint (m²)] x 100

GdT 08/12/16 - Added additional guidance on deducting area from asset footprint.

Asset performance eligibility criteria – Industrial assets - KBCN1471

The following guidance seeks to clarify how the eligibility criteria within the Scope section of the technical manual should be interpreted, particularly (though not exclusively) for industrial-type assets.

1) The asset must be a complete and finished structure.

A complete and finished structure means an enclosed, permanent structure with a roof and walls intended to accommodate people and/or processes.

a) Asset Performance

No more than 20% of the Gross Internal Area (GIA) can be classified as ‘unfitted’ at the point of submission. The assessment information provided must be correct at the point of submission to BRE Global for certification

To demonstrate that no more than 20% of the GIA (the assessed area) is ‘unfitted’, 80% of the GIA of the asset must be ‘ready for occupation’. This means it must be in a finished state, ready for occupation, or already operating in the intended function/process. This ‘finished’ state could be a controlled environment for a manufacturing process, warm or cold storage, IT or other technical operation. Alternatively, this could be an unconditioned internal environment, such as storage or packing and where most likely the only service fitted is electric lighting.

The requirement for 80% of areas to be operational or ready for occupancy applies to the total assessed area, including areas fitted out for processes and spaces conditioned for human occupancy.

2) The asset must contain occupiable or occupied space(s) which is designed to be continuously occupied for 30 minutes or more per day by a building user.

This is required to assess some criteria and award credits relating specifically to human occupation.

In order to demonstrate that a space is designed to be continuously occupied for 30 minutes or more per day by building users these spaces must be conditioned for human occupation and provided with basic services. Some examples of asset areas that meet this definition are offices, homes, retail, leisure areas which have ventilation, light and energy and water supplies, e.g. heating and/or cooling and access to a toilet and hand washing facilities.

However, process-based assets, which have any areas that are environmentally controlled by building services systems for human occupation OR processes, are eligible for assessment.

a) Asset Performance

An asset not yet occupied can still be assessed.

Provided that it meets the criteria above and is ready for occupation

09 Aug 2021 Eligibility Criteria relating to occupied space updated

Asset performance eligibility criteria – Self-storage assets - KBCN1514

The following guidance seeks to clarify how the eligibility criteria within the Scope section of the technical manual should be interpreted for Self-Storage assets.

Defining self-storage assets

Self-storage provides space for individuals to rent and store their personal or business belongings. The storage space - also referred to as storage units - is typically rented on a month-to-month basis. This space will make up the most space for any self-storage asset type.

Typical Scenarios:

- Local electric heating and cooling to front desk and small office space (relative to storage units)

- Hot water in the bathroom for staff or the public

- Space conditioning

- Storage units are naturally ventilated

- Storage units are mechanically ventilated but conditioned only to prevent extremes of temperature

- Storage units are mechanically ventilated and conditioned for temperature, and in some cases humidity

Scope

Eligibility Criteria

Criterion 1(a): no more than 20% of the Gross Internal Area (GIA) can be classified as 'Unfitted'.

As per

KBCN1471, this means that at least 80% of the GIA “must be in a finished state, ready for occupation, or already operating in the intended function/process. This ‘finished’ state could be a controlled environment for a manufacturing process, warm or cold storage, IT or other technical operation. Alternatively, this could be an unconditioned internal environment, such as storage or packing and where most likely the only service fitted is electric lighting.”

Criterion 1(b): no more than 20% of the Gross Internal Area (GIA) can be classified as 'Vacant'.

This requirement would only apply to office or staff spaces within the Self-Storage asset rather than the storage units themselves. The Storage units must be in a condition ready to be leased but do not need to be occupied during the period of assessment.

Criterion 2: The asset must contain occupiable or occupied space(s) designed to be continuously occupied for 30 mins or more per day by a building user.

This is required to assess some criteria and award credits relating specifically to human occupation.

Within Self-Storage assets, office and amenity areas will meet this requirement. The Self-Storage space will also meet this requirement provided it has ventilation, light and energy and access to water supplies.

Criterion 2(b): The asset must have been occupied at least 12 months prior to the start of the assessment.

For Self-Storage assets “occupied” means that office areas must have been occupied and the storage units must be ready to be occupied 12 months prior to the start of the assessment.

Asset Type/Sub-type

This asset type shall be classified as

Industrial.

The asset sub-type shall be

Distribution and Storage.

Automatic control for basin taps – Multi-residential long-term stay assets - KBCN1587

Only taps that are specifically used in staff, communal or public hand washing basins are required to meet the automatic control requirements set out in Criterion 1.

These requirements do not apply to residents’ private sanitary facilities in residential long-term stay assets.

Benchmark energy performance value – clarification - KBCN1724

The benchmark energy performance value is a performance level which achieves the

median performance within a local energy performance standard's range of values.

Example

In the UK, assets are rated using Energy Performance Certificates (EPCs).

Assets are rated from A to G. The median performance is a D rating. The D rating itself represents a range of performance values.

The benchmark energy performance value is the value at the middle of the D rating.

27-Mar-2025 - Published.

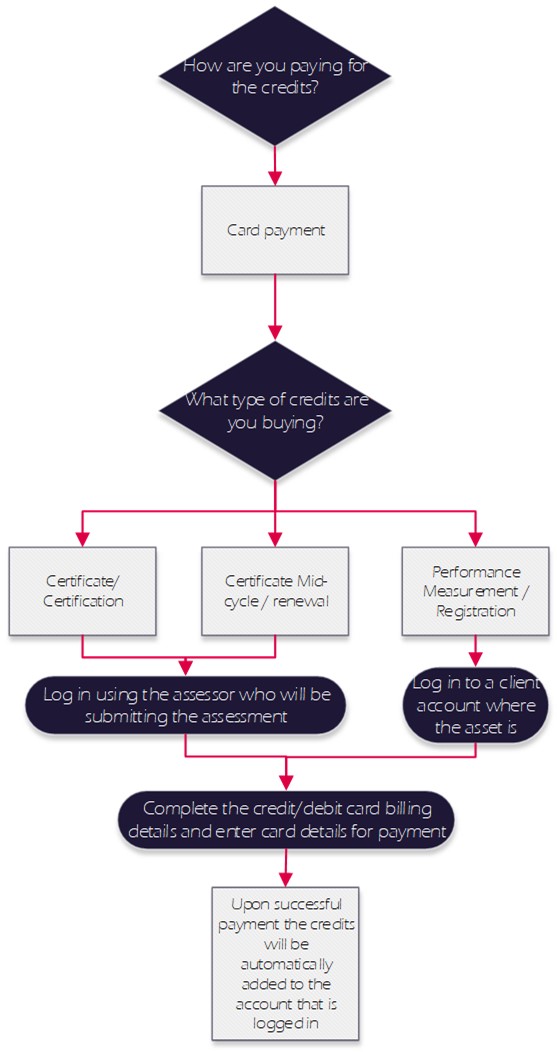

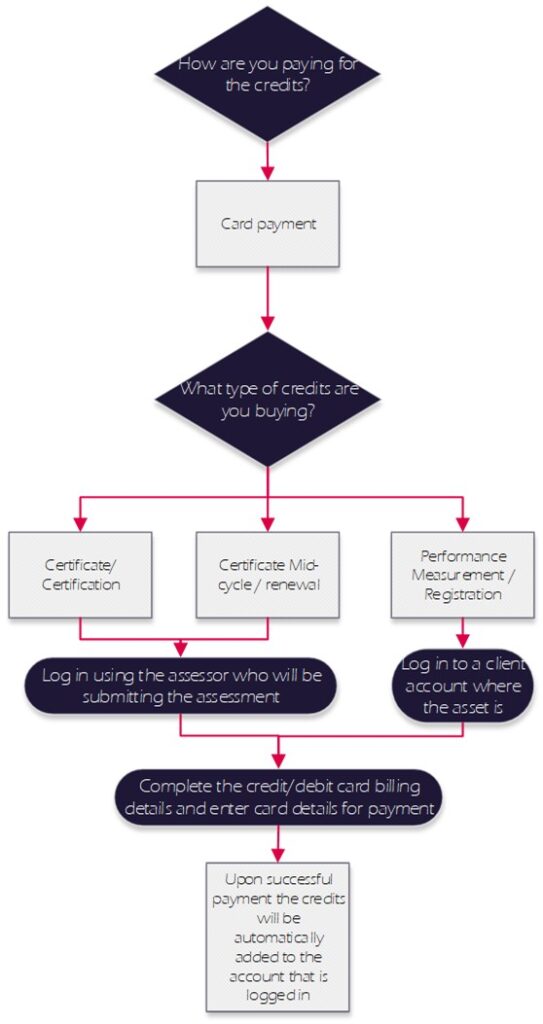

BREEAM In-Use credit purchases via card payment - KBCN1703

Online Payment – Credit/Debit card

The quickest route to obtaining BREEAM In-Use International credits for Measurement, Certification, Renewal and Mid-cycle certification, is to purchase these online and paying by credit/debit card. On successful completion of payment, the credits will be automatically allocated to the account who is logged in.

BREEAM Projects

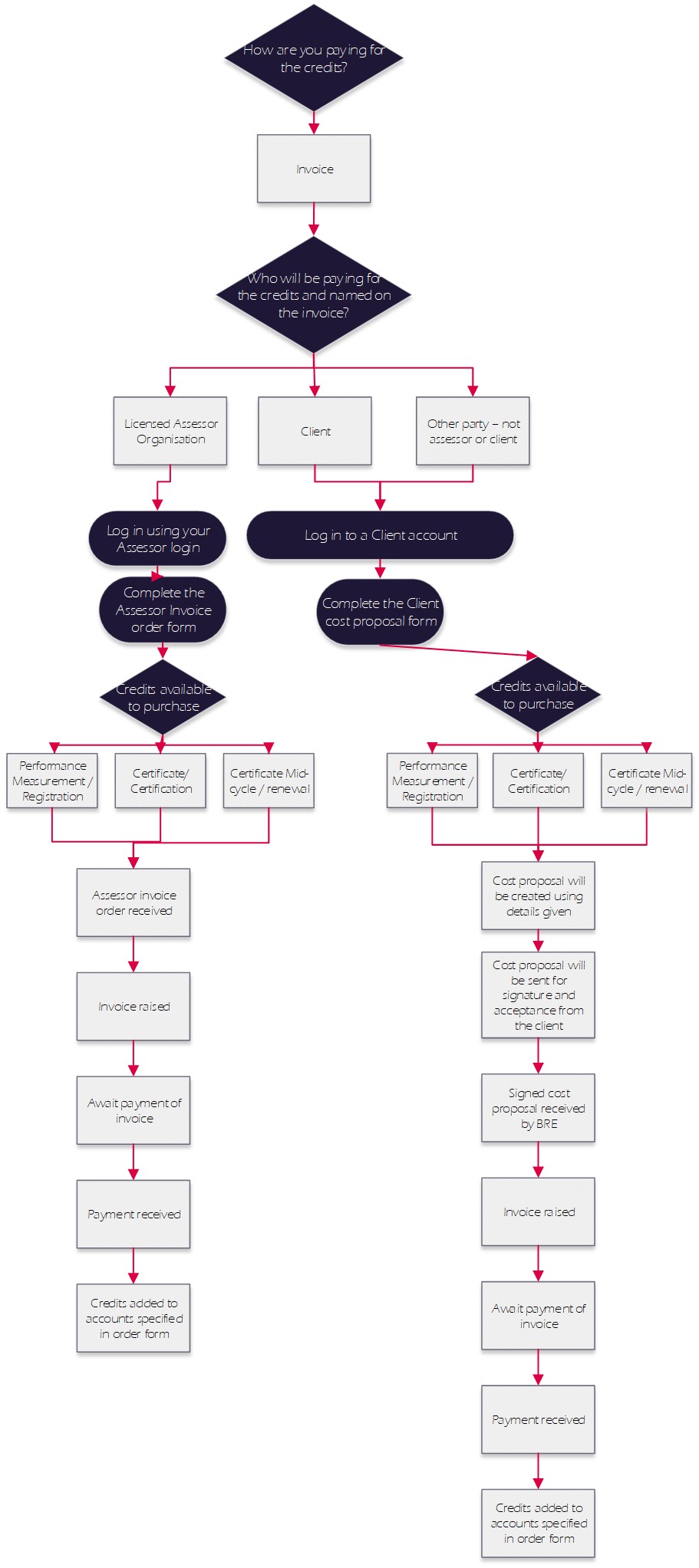

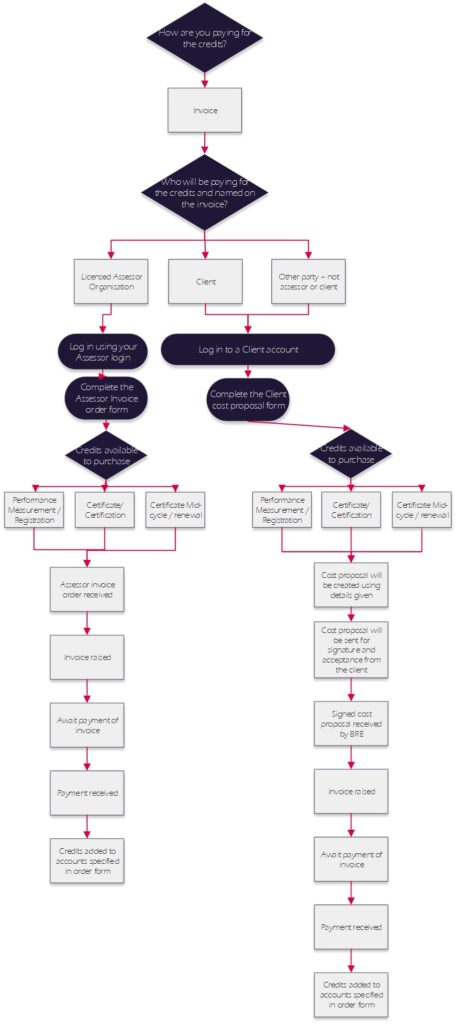

BREEAM In-use credit purchases via invoice payment - KBCN1704

Invoice Payment

If you are unable to purchase credits online using the card payment option, these can be processed via an invoice. You can select invoice on the ‘

Purchase credits‘ page within BREEAM Projects and complete the online request form. The request should be completed via the account who will be signing the cost proposal and receiving and paying the invoice. Further instructions and conditions are detailed within the request forms.

BREEAM In-Use Platform Migration – FAQs - KBCN1598

- Why have we made this change?

This is intended to provide a better user experience for both Clients and Assessors. The BREEAM Projects platform is faster and more stable than the BREEAM In-Use platform, reducing the risk of data loss. Unifying our schemes on a single platform will also allow us to be provide new features that can benefit all users.

- Will this change the current process?

There are some small changes to the appearance and functionality of the system and how you access the platform. However, this should not result in a significant change to how you work.

- Will this improve Operational or QA timescales?

Currently, the QA workflow for BREEAM In-Use assessments is primarily a manual process. After its migration onto the BREEAM Projects platform, the QA process will be carried out using the online tool, leading to improved efficiency in the QA assessment workflow and more streamlined processing of QA submissions.

- Will my login details change?

There will be no change to the login details for either BREEAM In-Use or BREEAM Projects users.

- Do I need additional training to use the new system?

We have designed the tool to maintain the functionality of the BIU platform. There will be some differences in the user interface, however additional training should not be necessary.

We will be sharing a system user guide in June 2023 for further support.

- Will active assessments be moved over?

Yes, assessments that are currently in-progress will be moved over.

- Will previously certified assessments be moved over?

Yes, assessments that are already certified will be moved over.

- Will I be able to see the evidence for all my assets in the new platform?

All the assets and evidence will be transferred to the BREEAM Projects platform and will work just as they did in the BREEAM In-Use platform.

However, please remember that the BREEAM License terms and conditions require Assessor organisations to maintain complete and accurate records of the assessment documentation for a period of ten years.

BRE only uses the evidence provided for the purpose of auditing and making a certification decision. We do not keep all assessment evidence once certification has been completed. Please ensure that you maintain your assessment records locally to prevent loss and to meet BRE’s terms of service.

- Will my existing credits within the BREEAM In-Use platform be moved over?

Yes, all existing credits within the BREEAM In-Use Platform will be moved onto the BREEAM Projects Platform as part of the data migration process.

- Will I be able to still access BIU platform after migration?

No. The BREEAM In-Use platform will be retired after the migration has been completed.

- Is the BREEAM Projects platform available in different languages?

Yes. There is an option to switch languages within the platform. This will change the display language of the interface and, where supported, within the technical guidance This will be available in the following languages:

- English – UK

- Chinese

- English – USA

- Norwegian

- Will it be possible to request an invoice for BIU credits in BREEAM Projects?

The payments process for purchasing BREEAM In-Use credits will not change. It will still be possible to purchase BIU credits using a credit/debit card, as well as being able to request an invoice via a cost proposal.

- Is the log in process the same for Clients and Assessors?

Yes, the process to log in is the same for clients and assessors. Each will use their existing credentials to log into BREEAM Projects. The tool will then identify the user and display the relevant pages.

- How do I access BREEAM Projects?

You can access BREEAM In-Use using this BREEAM Projects link:

https://tools.breeam.com/projects/login.jsp

- How do I log in from the USA or China?

Our Clients and Assessors in the USA or Chinese markets will be able to log in using the same login credentials that they currently use on the BIU Platform. They will also be provided with an option to switch the language within the tool.

- Will I have the ability to work in local currencies?

No additional currency support has been added to the platform as part of this migration.

- Will the terms of use change when we move to the Projects Platform?

All users, when accessing BREEAM Projects for the first time, will be required to agree to our ‘Terms of Use’ for the system. These Terms will not be too different from the existing ‘Terms of Use’ within BREEAM Projects and BREEAM In-Use platform. Whenever updated ‘Terms of Use’ are issued, users will be prompted to read and accept these before accessing the system.

- How do I contact BREEAM for support?

Assessors are encouraged to submit all enquiries using the

webform, which can be found via the

Assessor Support tab in BREEAM Projects. This provides drop-down menus to select the Department/Area and to choose further options, to ensure that your enquiry goes to the correct team.

Note: To help us provide an efficient service, Assessors are required to submit all technical queries using this webform.

Clients and other interested parties may continue to contact us by emailing the dedicated BREEAM In-Use email address:

breeaminuse@bregroup.com

19. How do I upload evidence on BREEAM Projects?

Please follow this link to view guidance:

Updated Process for Uploading Evidence

28 July 2023 FAQ 19 added

BREEAM Projects – basic asset details – asset constructed over different years - KBCN1626

Where different parts of the asset have been constructed over different years, in Basic Asset Details enter the year representing the largest proportion of floor area.

For example, if 60% of the asset area was constructed in 2008, and 40% in 1993, use '2008' as the year of construction.

Calculating the percentage of tenants - KBCN0805

Where calculations are undertaken to determine the percentage of tenants covered by a compliant green lease agreement, only those tenants that are part of the assessed area must be taken into account. Where tenants are not part of the BREEAM In-Use assessment, they must be excluded.

Please note: the calculation for the percentage of compliant tenants must be based on the number of tenants, not on the floor area.

Campus or campus-type developments – Entrance to consider - KBCN1726

For assessments on sites with multiple buildings (e.g. education campus, business or industrial parks):

- Distances to amenities and public transport nodes can be measured from the site’s main entrance if ≥80% of buildings are within 1000 m. Otherwise, use the assessed building’s main entrance, and in such cases, where multiple buildings are included, calculations must always be based on the worst-case scenario (the entrance furthest from the node or amenity)

- Where the site has more than one main entrance, either entrance may be used for the calculation.

Purpose: To ensure fair assessment on large sites and to encourage the provision or location of amenities and public transport nodes within or at the periphery of the site.

Note: wording update for clarification and including BIU

Car sharing group - KBCN1510

The term, ‘car sharing group’, as a sustainable transport measure, may be interpreted differently. For the purposes of the BREEAM Standards, therefore, the following additional guidance should be applied, to support assessors’ understanding of the criteria, when determining compliance.

Aim:

The aim of this measure is that the asset’s management establishes, promotes and administers a process which encourages building users to share private car journeys to and from work, thus reducing the number of cars used for this purpose.

Principles:

A car sharing group will, generally:

- Be available to all building users who normally travel to work by private car

A car sharing group is not:

- A vehicle hire/loan scheme

- Intended to offset journeys which would otherwise have been made by public transport or active travel modes (e.g. walking or cycling)

The criteria do not prescribe what terms and conditions should be implemented and, whilst the above principles should generally be followed, specific arrangements may vary.

However, evidence and justification must always be provided to demonstrate that the above ‘Aim’ is met.

Carbon dioxide sensors – Alerts - KBCN1868

Criterion 1 requires CO2 sensors to:

'Visibly or audibly alert the asset owner or manager or users of the space when carbon dioxide levels exceed the recommended set point.'

This requirement can be met by an automatically generated email or other message format, provided it is demonstrated that such messages will be delivered to the appropriate person/people within a reasonable time.

This meets the intent of the criterion and may, in some cases, be a more appropriate solution.

Carbon dioxide sensors – Erratum - KBCN1636

The question table for this issue should read as follows:

| Credits |

Answer |

Select a single answer option |

| 0 |

A |

Question not answered |

| 0 |

B |

No |

| 2 |

C |

Yes, in occupied spaces subject to large and unpredictable or variable occupancy patterns |

| 4 |

D |

Yes, in all occupied spaces |

This will be updated in the next reissue of the technical manual

Carbon monoxide detection – Combustion appliances located outside - KBCN1586

Where all combustion appliances are located outside in the open air, no flues pass through an occupied space and there are no enclosed parking areas, the associated credits can be filtered out as per Criterion 1.

Centralised air handling units (AHU) - KBCN0941

The requirements of the:

- Second sub-metering credit (New Construction).

- Issue (BREEAM In-Use).

do not apply to centralised AHUs, where it is not technically feasible to sub-meter energy use by separate functional, tenanted or floor areas.

The credit(s) will be assessed based on the remaining applicable energy uses.

06-Mar-2024 - Scheme applicability extended to V6.

Clarification – access to daylight - KBCN1648

Q11 of this issue asks 'what percentage of lit asset floor area has access to daylight?'

For this issue, 'access to daylight' means:

Spaces daylit from the side

- Is within 8m of a wall with openings that allow daylight in AND

- Openings comprise ≥ 20% of the wall area, as viewed from the inside.

For windows, the opening size is defined by the inside edge of the window frame, ignoring any transoms or mullions in the glazed area itself.

Spaces daylit from above

- Any spaces, or parts of a spaces illuminated by overhead openings, light tubes, or other daylighting strategies.

Where the daylighting strategy only covers part of a space, the assessor can use their judgement to define which areas have 'access to daylight' based on the specific design and lighting conditions.

Clarification – percentage of end uses - KBCN1650

This percentage is measured by the energy consumption (kWh) of significant energy uses, not by the number of end uses.

Clarification – reasonable timescale for refrigerant replacement - KBCN1733

If the asset targeting Answer D with a future commitment to replace refrigerants, these must be replaced within

3 years.

BREEAM In-Use assesses the current performance of an asset, and does not recognise far-future commitments. 3 years is the period of a single BREEAM In-Use certification cycle, and it is intended that any replacements are made during this current cycle.

28-Apr-2025 - Published.

Clarification of ‘Hazardous Chemical’ - KBCN1111

A 'hazardous chemical' can be considered to be any substance that is not found naturally in the environment, which has the potential to cause damage to the environment or the health of the building occupants (e.g. oil, fuel, solvents, pesticides, biocides, etc.).

Combined sub-metering – electric space / water heating and small power - KBCN00068

For bedrooms and associated spaces in:

- Multi-residential or residential institution building types (New Construction).

- Hospitality or supportive housing asset types (BREEAM In-Use).

It is acceptable for an electric space or water heating system to be combined with lighting and small power, provided that sub-metering is provided for each floor plate or other appropriate sub-division.

For these asset types, sub-metering electric heating in multiple bedrooms may be costly and technically challenging. Where occupants have individual control but are not responsible for paying the utility bills, the building manager may have little influence on their energy consumption. Therefore, sub-metering electric heating would provide little or no benefit in meeting the aim of the issue.

06-Mar-2024 - Scheme applicability extended to V6.

15-Dec-2023 - Title updated to clarify that this approach can be applied to both space heating and domestic hot water heating, where appropriate.

Combined system for heating / cooling and domestic hot water - KBCN0329

It is permissible to have combined metering for a shared on-site or district system that combines heating / cooling, and domestic hot water generation.

In all cases, justification is provided in the QA report for the combined metering, and explains why it is not technically feasible to provide separate meters.

21-Sep-2022 Applicability of KBCN added to BIU V6. Amended to include district heating and cooling networks.

Compliance: Applicability of criteria to scheme’s previous versions - KBCN0430

Criteria set for a scheme version are not applicable retrospectively to previous versions.

Condition survey – refurbishment in the last 5 years - KBCN1522

Where an asset has been refurbished, refurbished elements listed in criterion 2 can be excluded from the condition survey if:

- The refurbishment was carried out less than 5 years ago.

- The refurbishment addressed any and all major defects with the element.

- The records of the refurbishment allow asset management to effectively maintain that element.

The intent of Rsc 01 is to give asset management a complete understanding of the condition of the asset. The requirement for 5 years is to make sure that this information is relatively up-to-date, and allows effective maintenance of the asset and management of any minor defects.

All example scenarios below assume that the refurbishment was carried out less than 5 years ago. Any refurbishment works carried out more than 5 years ago must follow the full criteria of this issue.

[accordion]

[accordion_block title="Scenario 1"]

A major refurbishment to a Commercial asset covered and effectively documented refurbishment to:

a. Structure.

b. Mechanical components.

c. Electrical components.

d. Plumbing.

e. Fire protection.

It did not cover:

f. Communications and life safety systems.

g. Health and safety conditions.

All major defects were resolved.

Credits for the condition survey, and for rectifying defects are awarded based on elements f. and g. only.

[/accordion_block][accordion_block title="Scenario 2"]

A major refurbishment has covered and documented all items in criterion 2. All major defects were resolved, but there are some outstanding minor defects that are being monitored and maintained by asset management.

BIU V6: This issue is filtered out as per criterion 1.

BIU 2015: The relevant credits are awarded.

Minor defects are common after major building or refurbishment works, and typical building contracts provide a period for the resolution of minor defects. As long as major defects are resolved by the refurbishment, and asset management are aware of and managing minor defects, these items can be excluded from the condition survey.

[/accordion_block][accordion_block title="Scenario 3"]

A major refurbishment covered all elements, but there is no record of the refurbishment of mechanical and electrical components.

A condition survey covering these items is required. Relevant credits are awarded for surveying and addressing any defects for these elements.

[/accordion_block]

[/accordion]

Control of glare from sunlight – hotel rooms - KBCN1087

The primary function attributed to hotel rooms is that of a bedroom and as such, lighting and resultant glare are not considered to be problematic for these spaces.

The only exception to this is where designated additional office space is provided. In these circumstances it is the role of the assessor to determine if individual spaces should be determined as ‘relevant building areas’ in accordance with guidance provided.

Glare control criteria apply to building areas where lighting and resultant glare could be problematic for users.

01 Nov 2023 - Applicability to BIU V6 Commercial confirmed

This KBCN aligns with KBCN0666 from UKNC 2014

Control of glare from sunlight – Use of EN 14501 to demonstrate compliance for blinds - KBCN1737

The criteria set the following requirements for blinds:

- an openness factor of 1% or less and

- a light transmission value less than 10%

Alternatively, Class 3 and Class 4 solar protection devices in Table 7 of EN 14501:2021 can be considered as meeting the BREEAM criteria.

The following meets Class 3 within EN 14501 and can, therefore, be considered compliant:

- an openness factor of 1% or less and

- a light transmission value of 10% or less

02 Sept 2025 - KBCN reworded to clarify the intent.

Converting water consumption into litres per year from new EU energy labels - KBCN1548

The following conversion factors may be used to convert the water consumption on new EU energy labels from litres per cycle (L/cycle) into litres per year (L/year):

Dishwasher: multiply water consumption figure on EU energy label by 280 (to go from L/cycle to L/year).

Washing machines: multiply water consumption figure on EU energy label by 220 (to go from L/cycle to L/year).

This follows equivalent guidance for converting energy consumption (see

KBCN1462).

25 Aug 2023 - Correction to 'typo error' for dishwasher conversion factor - previously shown as 208, now corrected to 280.

Cycle facilities – Separate showers within shared gender-specific (single gender) facilities - KBCN1601

Cultural norms and expectations in relation to privacy may vary. The guidance on providing separate showers in the above situation is, therefore, clarified as follows:

Where showers are not divided into individual cubicles, or are only partially separated, this does not preclude compliance. However, the assessor must be satisfied and provide justification that the arrangements are in line with local custom and appropriate to the building type and the demographic of building users.

Cycle spaces – Minimum and maximum requirements - KBCN0637

These remain applicable where the 50% reduction allowed for building locations with a high level of public transport accessibility is in effect.

This means that, for instance, a large retail will still need to provide at least ten customer cycle storage spaces and could meet compliance with a maximum of fifty.

22-Nov-2023 Scheme applicability updated.

18-May-2017 Previous KBCN on large retail adapted to include any minimum requirement for cycle storage spaces.

Cycle spaces – Folding bicycles and scooters - KBCN00024

The provision of cycle storage that is only suitable for folding bicycles or scooters is not compliant.

Providing reduced storage space for folding bicycles or scooters in place of compliant cycle storage may limit future travel options.

14 03 2018 Wording clarified and reference to scooters included.

Cycle storage – 50% reduction applies to all users - KBCN1631

Where a 50% of reduction in required cycle storage spaces is allowed for any reason (for instance, for meeting a threshold for good public transport accessibility), this applies to

all asset users. This includes staff, and any applicable users such as customers, visitors or residents.

However, any minimum or maximum requirements remain the same. See

KBCN0637.

This principle aligns with BREEAM New Construction and Refurbishment and Fit-Out.

Cycle storage – Multi-residential long-term stay - KBCN1592

For the purposes of calculating the cycle storage requirements, residents should be considered as 'staff'.

Cyclists’ facilities – Combining different facilities - KBCN0683

Cyclists' facilities can be combined, provided that all relevant compliance requirements are met and it is demonstrated that there is no conflict impacting on their use. For example, compliant showers can be combined with compliant lockers in one room, subject to the principle below.

For combined facilities to count as multiple facilities, they must be capable of being used independently of each other at the same time (where relevant) with reference to any space requirements, access, gender and privacy issues.

11 Jan 2023 - Applicability to BIU V6C confirmed

10 Feb 2022 - Updated to clarify that facilities can be combined where there is no conflict.

Cyclists’ facilities – Matching additional cycle spaces - KBCN00093

The minimum number of showers/lockers/changing facilities required for BREEAM compliance is determined by the minimum number of compliant bicycle spaces required, not by how many total compliant bicycle spaces have been provided. Where more than the minimum number of compliant cycle spaces has been provided, there is no requirement to provide more than the minimum number of showers/lockers/changing facilities.

01 Feb 2022 - Wording clarified and applicability to BIU V6C confirmed

Cyclists’ facilities – Multi-residential / residential institutions - KBCN0967

Where there is a BREEAM requirement for residents, compliant facilities within their accommodation can be considered as cyclists' facilities. Separate facilities for staff must be provided as required to achieve compliance.

22 Aug 2023 Applicability to BIU V6 Commercial confirmed.

Cyclists’ facilities – Within toilet facilities - KBCN00050

To comply with the criteria for cyclist facilities, showers should not obstruct the use of other facilities. Where a shower is located in a room with a WC, this cannot be considered compliant, unless it can be unequivocally demonstrated that the WC is provided over-and-above the requirements of relevant standards or regulations for general and disabled WCs.

To ensure that there is no conflict between the use of general or disabled WCs and the use of cyclist facilities.

25.10.18 KBCN reworded to improve clarity.

Dedicated transport service - KBCN1823

A dedicated transport service, such as a dedicated bus, coach, or minibus, provided or managed by the building owner or management, can be considered for any building type with a fixed usage pattern. The dedicated transport must provide a transfer to the local population centre or public transport interchange, or it may be a door-to-door service.

Generally, a dedicated service must be available to all regular building users. However, for primary and secondary schools, a dedicated service available to students only can be considered compliant

Dedicated transport service - KBCN1823

A dedicated transport service, such as a dedicated bus, coach, or minibus, provided or managed by the building owner or management, can be considered for any building type with a fixed usage pattern. The dedicated transport must provide a transfer to the local population centre or public transport interchange, or it may be a door-to-door service.

Generally, a dedicated service must be available to all regular building users. However, for primary and secondary schools, a dedicated service available to students only can be considered compliant

Determining boiler efficiency - KBCN1223

The boiler efficiency should be based on the Higher Heating Value (HHV) or the Gross Calorific Value (GCV). Where the information related to the efficiency of the boiler is only available in Lower Heating Value (LHV) or Net Calorific Value (NCV), it will need to converted using the following formula:

HHV = LHV x 0.9

GCV = NCV x 0.9

District heating / cooling / hot water – entering data into the Online Platform - KBCN1536

For assets which use district heating / cooling / hot water, information on the district systems are entered into Ene 09a and 09b.

In Ene 05 / 06 / 09, answer 'no' to first question

"Is space heating / cooling / hot water generated on-site?" then navigate to:

- Ene 09a to answer questions on district cooling.

- Ene 09b to answer questions on district heating and hot water.

A district heat network will also provide hot water, so information on the system which provides both is entered into Ene 09b.

The Online Platform differs from the manual structure, however it does not affect scoring in any way. All data entered contributes to the asset energy calculator.

Assets with on-site and off-site systems

Only answer questions on the system which provides the most signifcant heating or cooling to the asset. If an asset includes both on-site and off-site systems, choose the one which delivers the most energy annually.

Durable and resilient features – Features not present - KBCN1547

The requirements of Rsl 04 aim to minimize the frequency of building component replacement. Options D, E and F relate to specific features that are vulnerable to damage through the building's operation. Therefore, if it can be demonstrated that an asset does not include any such features, this requirement can be considered met, because there is nothing to protect.

Evidence confirming the above must be referenced and provided in the assessment.

It is unlikely that Option C will not apply in a commercial asset. However, if an assessor believes this to be the case, they should contact BREEAM Technical with full details and justification.

20 Oct 2023 - Applicability to BIU V6 Residential removed - Options can be filtered out where not applicable.

14 Dec 2022 - Updated to include Options D and E, in addition to the reference to Option F.

Efficiency data for local electric instantaneous hot water systems - KBCN1736

When inputting the hot water generation efficiency data for local electric instantaneous hot water systems, this may be input as 1 in line with the SBEM Methodology.

Electric Vehicle (EV) Charging – Shared Parking for New Buildings, Extensions, and Phased Developments - KBCN1827

The required number of EV charging points must be based on the total number of parking spaces that

serve the assessed building. This total includes both

existing spaces and

any new spaces associated with the project.

Where parking is shared across a wider site, the “associated” number of spaces refers to the amount of parking the assessed building is expected to rely on for its occupants. A

proportional allocation calculation must be used to determine this number.

Example:

If a project sits on a site with 1,000 shared spaces but the new building’s occupancy requires only 100 spaces, the EV requirement is calculated based on

100 spaces, not the full 1,000.

- General Requirements

- Defining the parking that counts. Use a proportional allocation method to determine how many spaces in a shared car park are associated with the project.

- Short-stay exclusion: Short-stay spaces with a maximum stay of 15 minutes (e.g., pick-up/drop-off bays) are excluded from the EV calculation.

- EV Charging points location: EV charging points should be installed as close as possible to the building’s main entrance to ensure convenient access for the building users.

- Existing infrastructure: Existing EV charging points in a shared car park can only be counted when:

- They exceed the BREEAM requirement for the buildings they were originally installed to serve,

- They meet current BREEAM requirements, and

- They form part of the new project’s allocated parking.

- No “legacy” exclusions: Existing parking spaces cannot be excluded simply because they predate the BREEAM assessment. If the spaces serve the assessed building, they are in scope.

- Operational policy. It is recommended, but not mandatory, that building management implement operational measures (e.g., signage, permits, digital access controls) to help ensure that EV spaces are used by the intended building users.

- New Buildings on a Site or Extensions

- Calculation basis for new buildings or extensions, EV requirements must be based on the total parking demand associated with the project, including both existing associated spaces and any new spaces created.

- Proportional allocation formula

- Determine the project’s share of the total site parking using either GIA or occupancy.

- Allocated project parking = Total site parking × (Project GIA ÷ Total GIA), OR

- Allocated project parking = Total site parking × (Project occupancy ÷ Total occupancy)

- Phased Development

- Current Phase: The EV calculation should be based on the parking demand of the phase under assessment, including the existing infrastructure and any new parking spaces delivered in that phase.

- Existing Infrastructure: EV charging provision installed in previous phases may count towards compliance where it meets the required threshold for the current phase

- Future Phases: Provisions in future phases may be counted only if secured by a legally binding commitment (such as a signed contract or planning obligation) with a confirmed delivery timeline.

Electric vehicle charging stations (EVCS) – Priority spaces - KBCN1429

The current criteria for EVCS do not address provision for priority spaces, such as those allocated to disabled use and car sharing.

The assessor and design team should, therefore, take a pragmatic approach to this and, where the overall number of required EVCS permits, an appropriate proportion of these should be provided for priority spaces. This will not be deemed as 'double-counting' as the number of EVCS required should be considered independently of other requirements.

The intent is that electric vehicle charging spaces are available to all building users (where possible).

Electric vehicle charging stations – Availability - KBCN1128

This option requires the number of electric vehicle recharging stations (EVCS) to be based on a percentage of the total car parking for the building.

To meet compliance, the intent is that recharging stations be available to all building users, including customers and visitors. However, where overall parking numbers are low, it may be difficult to effectively distribute the EV charging spaces between general users and priority groups.

In such cases, the design team must provide evidence that this aspect has been considered when locating the EV spaces, however, the decision on how to distribute these may be made by the client or, for speculative development, by an appropriate member of the design team.

In situations where parking is limited to priority spaces only, the above guidance still applies.

11 Jan 2023 - Applicability to BIU V6C confirmed

17 Sep 2022 - Updated to allow more flexibility in relation to how EV spaces are allocated

Electric vehicle charging stations – Short-term visitor spaces - KBCN1735

Where it can be demonstrated that parking spaces for visitors will only be used for short-term parking (a maximum of 15 minutes), these spaces can be excluded from the calculation for EV spaces.

This exclusion will typically apply to certain types of retail outlet, where visitors are, for example, collecting or dropping off orders. However, other situations can be considered, where justified.

Eligibility criteria – BIU International Residential V6 - KBCN1668

The Eligibility Criteria for BIU V6 Residential have been updated, and the guidance below supersedes Criterion 2 in the V6.0 technical manual:

Criterion 2)

a) Submission for certification must be a minimum of 12 months from completion of the dwellings.

AND

b) For a Part 2 assessment, 12 months’ utility consumption data must be available for a minimum of 80% of the dwellings.

AND

c) The asset must be intended to be a primary residence of the occupants.

Emergency lighting - KBCN0185

Maintained systems featuring emergency light fittings which are also used for normal operation, are assessed for this issue.

Non-maintained lighting which is only activated in an emergency can be excluded from the assessment.

NC / RFO / BIU V6 Ene 17: The aim of these credit(s) is to encourage and recognise energy-efficient fittings. Non-maintained emergency lighting will very rarely be activated and in such extremes the emergency requirements must not be compromised.

BIU V6 Hea 05: Flicker is eliminated from maintained systems only.

24-Jan-2024 - Scheme applicability updated to include BIU V6.

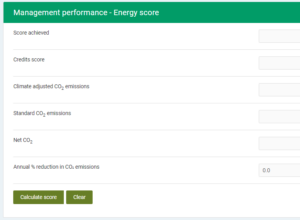

Ene 24 methodology - KBCN1613

This issue is scored based on % improvement relative to the

BIU V6 carbon benchmark and average annual improvement across the reporting periods.

[accordion]

[accordion_block title="BIU V6 carbon benchmark"]

Standard CO2 emissions:

Standard CO2 emissions: the tailored benchmark of a UK asset.

Climate adjusted CO2 emissions: the benchmark for International assets. It adjusts the UK benchmark to account for national and regional differences.

Net CO2: the actual CO2 emissions of the asset.

Annual reduction in CO2 emissions: the annual average % figure used to score credits in Ene 24.

[/accordion_block]

[/accordion]

Example scenario

An international BIU asset calculates the improvement in CO2 emissions across 2 reporting periods.

- CO2 emissions benchmark = 50 kgCO2e/m2 per year.

- 01-Jan-2020 to 31-Dec-2020.

CO2e emissions are 90 kgCO2e/m2 per year (1.8x the benchmark).

- 01-Jan-2023 to 31-Dec-2023.

CO2e emissions are 60 kgCO2e/m2 per year (1.2x the benchmark).

- Time between reporting periods: 3.0 years.

Calculation

- Improvement over 3 years = 1.8 - 1.2 = 0.6x improvement vs benchmark.

- 0.6 = 60%

- 60% / 3.0 years = 20%

The asset demonstrates a 20% average annual improvement vs the benchmark. It scores 3 exemplary credits.

How the calculation accounts for different reporting periods

Most assessments will report on multiple fuels in each period.

- Individual reporting periods for fuels may not align.

- Reporting periods may not begin or end at the same time each year.

[accordion]

[accordion_block title = "Calculating time between reporting periods"]

Time between reporting periods is measured in days (this is converted to years in the final calculation). Time is measured from the middle of each reporting period.

If more than one fuel is reported, the individual mid-dates for each fuel are combined through a weighting calculation. The mid-date is proportionally weighted towards fuels with larger associated CO2 emissions.

[/accordion_block]

[accordion_block title = "Maximum time between reporting periods"]

The maximum time between any reporting period is 1460 days (3 years 364 days) between:

- The first recorded consumption data in the 1st period, and

- The first recorded consumption data in the 2nd period.

These dates are

not weighted by fuel consumption.

[/accordion_block]

[/accordion]

Additional notes

- Erratum - Criterion 1. Assets where the 1st period was assessed under BIU 2015 must re-enter this consumption data into the BIU V6 Ene 24 calculator. This ensures a consistent calculation methodology for all BIU V6 assets.

- The baseline for measuring improvement (1st period performance vs benchmark) are actual asset emissions, not the benchmark. Asset CO2e emissions can exceed the benchmark in both the 1st and 2nd periods to target credits in this issue.

- The manual states that 3 years are required between periods (as this links to the BIU V6 certification cycle), however this is not a requirement for compliance. Assets can also target this issue where less than 3 years have passed (for instance after a mid-cycle certification). The calculator will adjust for the shorter gap between reporting periods.

Energy Consumption Reporting – common areas only assessment - KBCN1698

For assets where only the common areas are being assessed, the energy consumption targets and actual figures reported should be based on the energy within the assessed areas only.

Please note that where the asset does not have consumption data which covers the assessment area only, the BREEAM In-Use International Energy Allocation Calculator should be used when completing the Management Performance Energy Category.

Energy consumption reporting – Link to Man 04 - KBCN1612

The link to meeting compliance with Man 04, outlined in Ene 23 Criterion 1 is incorrect and should be disregarded.

Answer option D in Man 04 includes targets for Energy, Water and Waste. Whereas the intent of Ene 23 relates to targets for Energy only. This will be updated in the next reissue of the technical manual.

Enhanced waste collection in the asset - KBCN1528

Where the asset collects 6 or more unique residential waste streams on-site, answers G and H are available without the need for additional off-site collection points.

If the asset can provide enhanced waste collection and sorting on-site, then this is effectively the same as having a compliant collection point in the local area.

Example scenarios

[accordion]

[accordion_block title="5 waste streams on-site"]

An apartment building has compliant facilities or kerb-side collection for 5 residential waste streams. There is no collection for composting or garden waste.

The asset achieves the requirements for answer C only if all relevant criteria are met. There aren't enough waste streams to meet the threshold for answer G.

[/accordion_block]